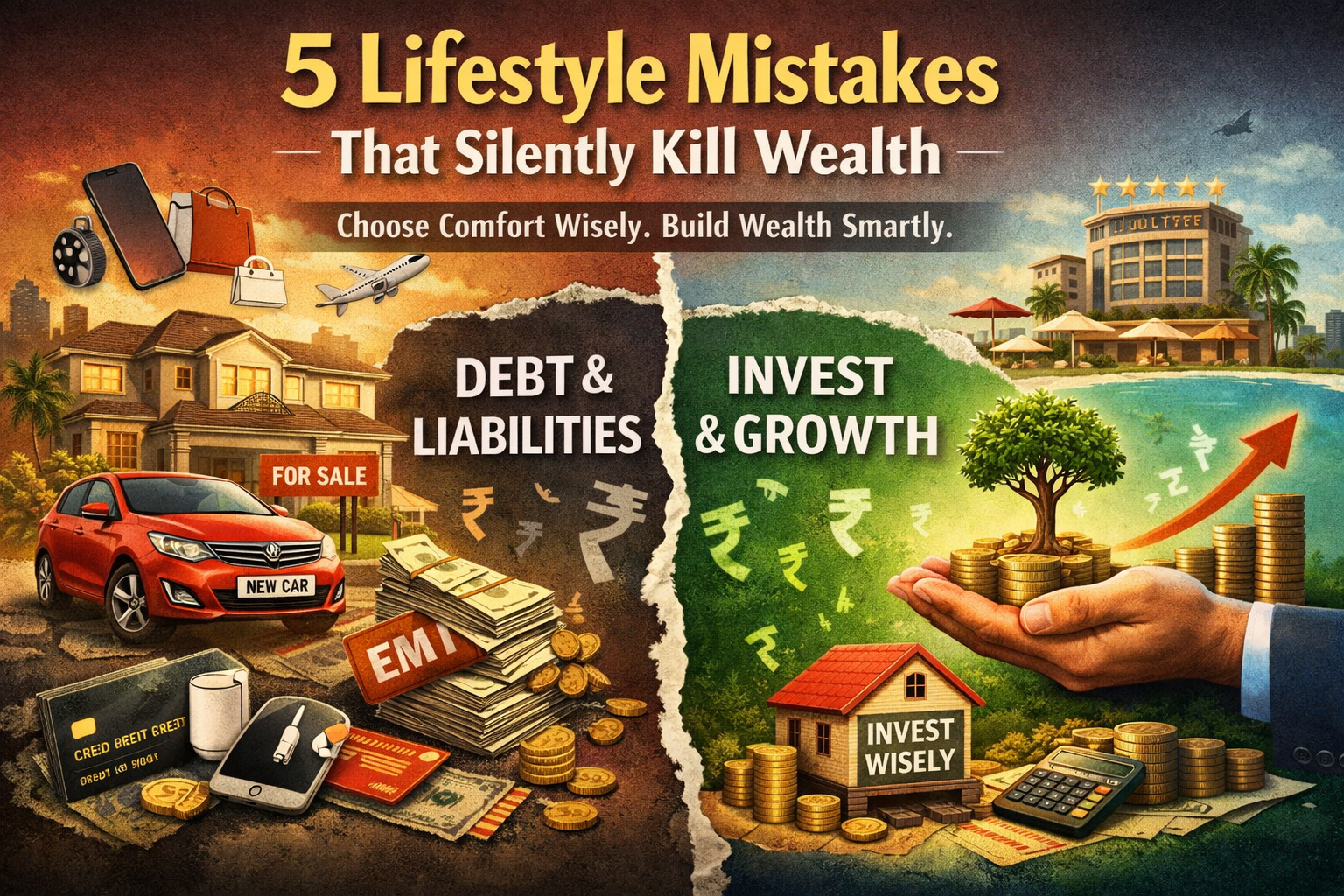

A Critical Perspective Before We Begin

Cars, houses, furniture, gadgets, and vacations are tools of comfort — not indicators of wealth.

A car is a tool to move from Point A to Point B

A house is a tool that provides shelter and safety

Furniture & interiors are tools for comfort

Technology is a tool for productivity

Vacations are tools for rest and mental refresh

When we forget their purpose, these tools silently turn into financial liabilities.

Every rupee saved by making rational choices here becomes investible capital. That same money, when invested wisely, compounds into a large asset over time — without any interest cost, unlike EMIs and loans.

1. Purchasing Brand-New Cars for Status

A car’s job is simple:

To take you safely from Point A to Point B.

The difference is not in comfort — it is in financial impact.

Example: New Car vs Second-Hand Car

Option A: Brand-New Car

Cost: ₹10,00,000

Loan tenure: 5 years

Interest rate: 9% p.a.

Monthly EMI: ₹20,758

Option B: Second-Hand Car

Cost: ₹5,00,000

Loan tenure: 5 years

Interest rate: 9% p.a.

Monthly EMI: ₹10,379

👉 Monthly EMI saved: ₹10,379

Now comes the real wealth decision.

If the Saved EMI Is Invested

Monthly SIP: ₹10,379(For the 1st five Years only)

Expected return: 15% p.a.

Investment period: 10 years

👉 Future value of investment:₹18.25+ lakhs (approx.)

After 10 years:

The car has depreciated

The comfort served its purpose

But the invested EMI has become a sizable asset

Same mobility. Completely different wealth outcome.

2. Buying Houses Beyond True Affordability

A house is meant to:

Provide stability

Offer peace of mind

Create security

When EMIs consume a large portion of income, the house stops being a comfort tool and becomes a financial burden.

Example: Overstretching vs Affordable Home

Option A: Overstretching the Purchase

House cost: ₹50 lakhs

Loan tenure: 20 years

Interest rate: 9% p.a.

Monthly EMI: ₹44,986

Option B: Affordable & Balanced Choice

House cost: ₹35 lakhs

Loan tenure: 20 years

Interest rate: 9% p.a.

Monthly EMI: ₹31,490

👉 Monthly EMI saved: ₹13,496

If the EMI Difference Is Invested

Monthly investment: ₹13,496

Expected return: 15% p.a.

Investment period: 20 years

👉 Future value of investment:₹1.79 crore (approx.)

3. Treating Furniture & Interiors as Assets

Furniture and interiors:

Add comfort

Improve aesthetics

But they:

Do not appreciate

Lose value over time

Have limited resale worth

Frequent upgrades drain savings

Many people repeatedly spend on:

Modular kitchens

Premium sofas

Designer interiors

Comfort should be functional. Excess should be invested.

4. Using Technology as a Status Symbol

Technology is meant to:

Improve productivity

Enable communication

Save time

Frequent upgrades driven by trends convert useful tools into financial drains.

The same money, if invested instead of upgraded, can compound silently into a meaningful corpus.

Let your money upgrade your future before upgrading your gadgets.

Vacations are tools for:

Mental refresh

Family bonding

Luxury experiences funded through EMIs or credit cards create:

Interest costs

Reduced investments

Post-vacation financial stress

Memories should not come with long-term repayment schedules.

A Powerful Question That Changes Every Financial Decision

Instead of asking:

“Can I afford this?”

Ask:

“How much of my future money am I committing by owning this?”

Affordability looks at today’s income.

Commitment looks at tomorrow’s cash flows.

This single shift in thinking leads to far more rational financial choices.

The Real Lesson

Smart lifestyle decisions do two things simultaneously:

Reduce interest-bearing liabilities

Create surplus for compounding investments

Over time, this gap between assets and liabilities decides who becomes wealthy and who remains financially stressed.

Final Thought

True wealth is not about denying comfort.

It is about deploying money where it grows instead of where it depreciates.

At PVR Advisory, we believe:

“Assets grow through compounding.

Liabilities grow through interest.

Wise choices decide which one dominates your life.”

Wealth is built quietly — one rational decision at a time.

Note: I written this article with an inspiration of this ideology from Charlie Munger & Warren Buffet.

Disclosure: Investments in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BSE and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors