Buying a home is one of the most emotionally fulfilling and financially significant decisions in life. However, without careful planning, this dream can turn into a long-term financial burden.

Whether you're a first-time buyer or upgrading to a bigger home, consider these 13 essential points before you commit to a property purchase or home loan.

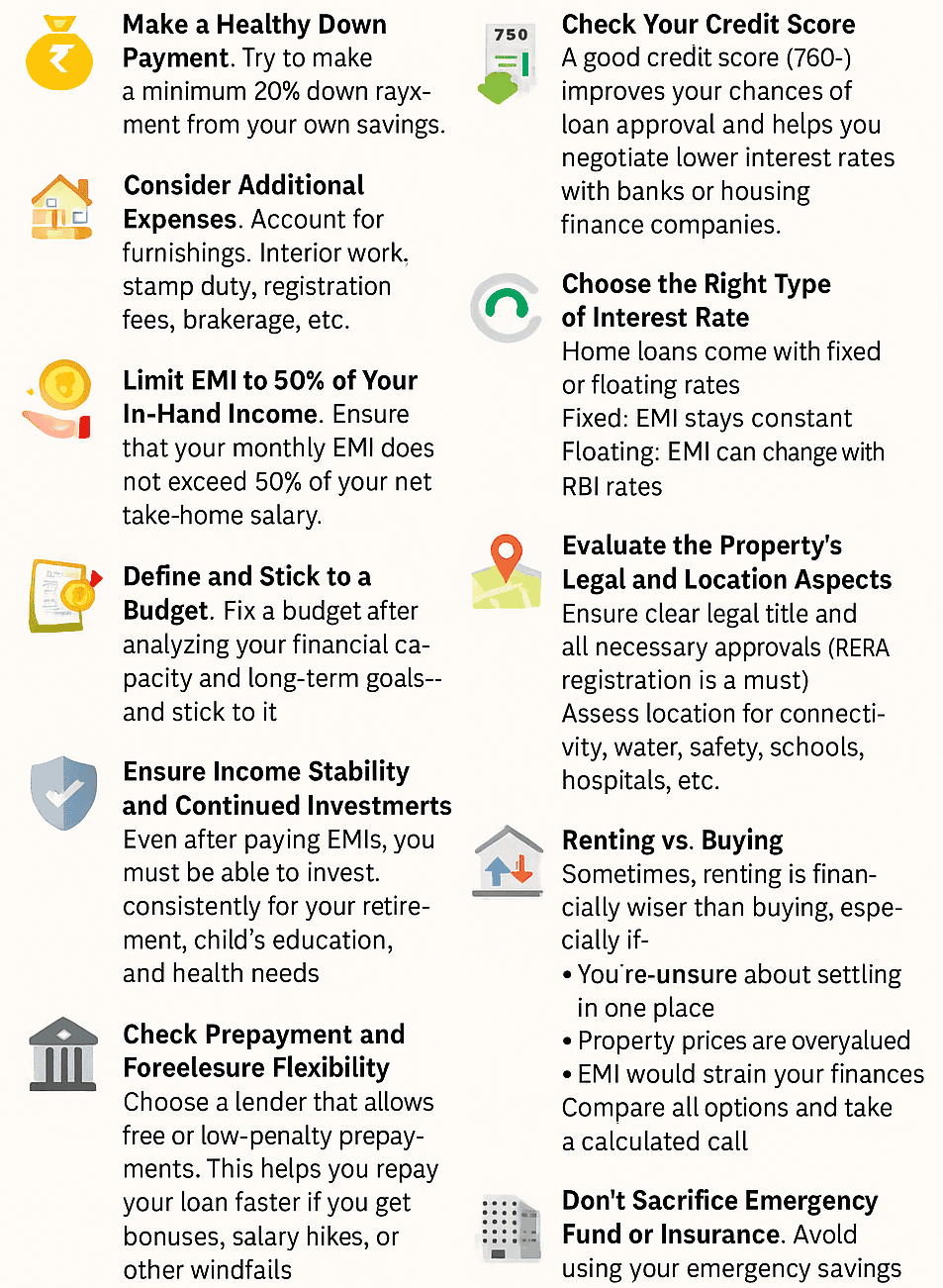

1. 💰 Make a Healthy Down Payment

Try to make a minimum 20% down payment from your own savings. This reduces your loan amount, lowers your EMI, and saves you a significant amount on interest over the years.

2. 💡 Consider Additional Expenses

Your home cost isn’t limited to just the property price. Account for furnishing, interior work, stamp duty, registration fees, brokerage, and other incidental expenses.

3. 📊 Limit EMI to 50% of Your In-Hand Income

Ensure that your monthly EMI does not exceed 50% of your net take-home salary. This ensures you still have room for living expenses, savings, and emergencies.

4. 📝 Define and Stick to a Budget

Avoid falling for properties beyond your affordability. Fix a budget after analyzing your financial capacity and long-term goals—and stick to it.

5. 📈 Ensure Income Stability and Continued Investments

Buying a house should not compromise your other life goals. Even after paying EMIs, you must be able to invest consistently for your retirement, child’s education, and health needs.

6. 📉 Check Your Credit Score

A good credit score (750+) improves your chances of loan approval and helps you negotiate lower interest rates with banks or housing finance companies.

7. 🔁 Choose the Right Type of Interest Rate

Home loans come with fixed or floating rates:

Fixed: EMI stays constant

- Floating: EMI can change with RBI ratesChoose based on your comfort with interest rate fluctuations.

8. ⏳ Select an Optimal Loan Tenure

Longer tenures mean lower EMIs but higher total interest. Choose the shortest tenure possible without compromising your lifestyle or emergency preparedness.

9. 📍 Evaluate the Property's Legal and Location Aspects

Ensure clear legal title and all necessary approvals (RERA registration is a must).

Assess location for connectivity, water, safety, schools, hospitals, etc.

10. 🏦 Check Prepayment and Foreclosure Flexibility

Choose a lender that allows free or low-penalty prepayments. This helps you repay your loan faster if you get bonuses, salary hikes, or other windfalls.

11. 🏘️ Renting vs. Buying

Sometimes, renting is financially wiser than buying, especially if:

You’re unsure about settling in one place

Property prices are overvalued

- EMI would strain your financesCompare all options and take a calculated call.

12. 🛡️ Don’t Sacrifice Emergency Fund or Insurance

Avoid using your emergency savings or discontinuing insurance policies for the down payment. You need backup funds and protection against life's uncertainties.

13. 🧱 Verify Builder Credibility (Especially for Advance Payments)

If you're buying under construction or paying in advance, always check the builder's background:

Track record of timely possession

Legal disputes or project delays

- RERA compliance and customer reviewsDon’t fall for discounts or promises without due diligence.

🔚 Final Word:

"House purchase is one of the biggest financial decisions you will make. Analyse your situation carefully before making any commitment of your future income."

Take a step back, assess your financial landscape, and take informed decisions rather than emotional ones. The right planning ensures your home remains a blessing, not a burden.

💼 Need Guidance?

At PVR Advisory, we help you:

Assess affordability

Plan EMIs smartly

Compare rent vs buy

Align your home decision with other financial goals

📞 Reach out today for an unbiased opinion before committing to a home loan.